It is more important than ever to really be aware of who you are working with. Scale Funding provides you phone access to our credit desk 40 hours a week & live online credit decisions 24/7, but some nights, weekends, or just for your own peace of mind, you might want some more details on a company you are looking to haul for. One of the fastest (and free-est) tools out there is SAFER, courtesy of the Federal Motor Carrier Safety Administration (FMCSA)

While the FMSCA branched off from the DoT right at the turn of the century, Safety and Fitness Electronic Records (SAFER) have been available online since 2004.

What is FMCSA’s SAFER system and why use it?

Q: What is FMCSA’s SAFER system and why use it?

A: It’s a federal database of carrier safety and licensing data—use it to vet partners and monitor compliance.

How does SAFER data support faster pay?

Q: How does SAFER data support faster pay?

A: Clean safety profiles reduce disputes and insurance issues that can delay payments.

Scale Funding’s recommendation is to work only with brokers who:

- Have been in business for a full year

- Have active authority

- Are fully insured and licensed

Most of that may seem like common sense, but there has been a rise in companies that pop up specifically to get around those rules. On the FMCSA website, you can see these details by going HERE and entering the DOT or MC number of the company in question.

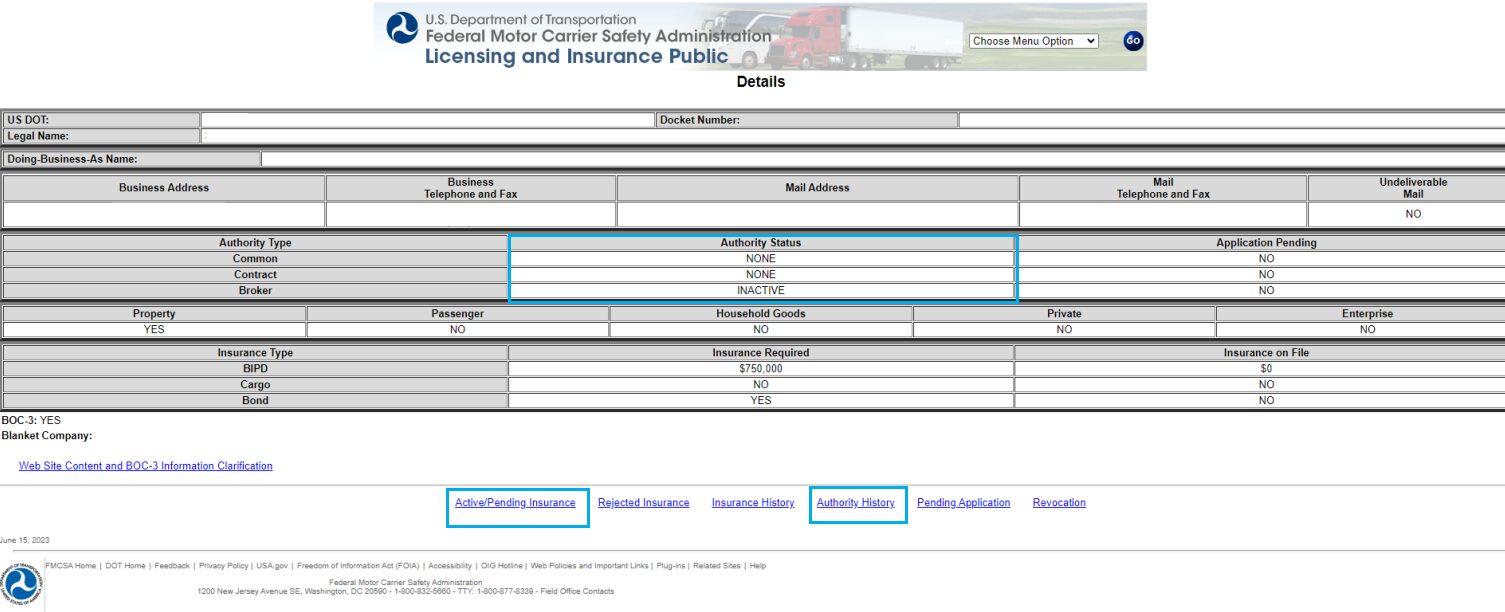

There are 3 main sections you want to look at here. First of all, Authority status. Obviously, if their status is inactive, or they are trying to broker you a load with only common authority, Scale Funding would recommend turning down that load.

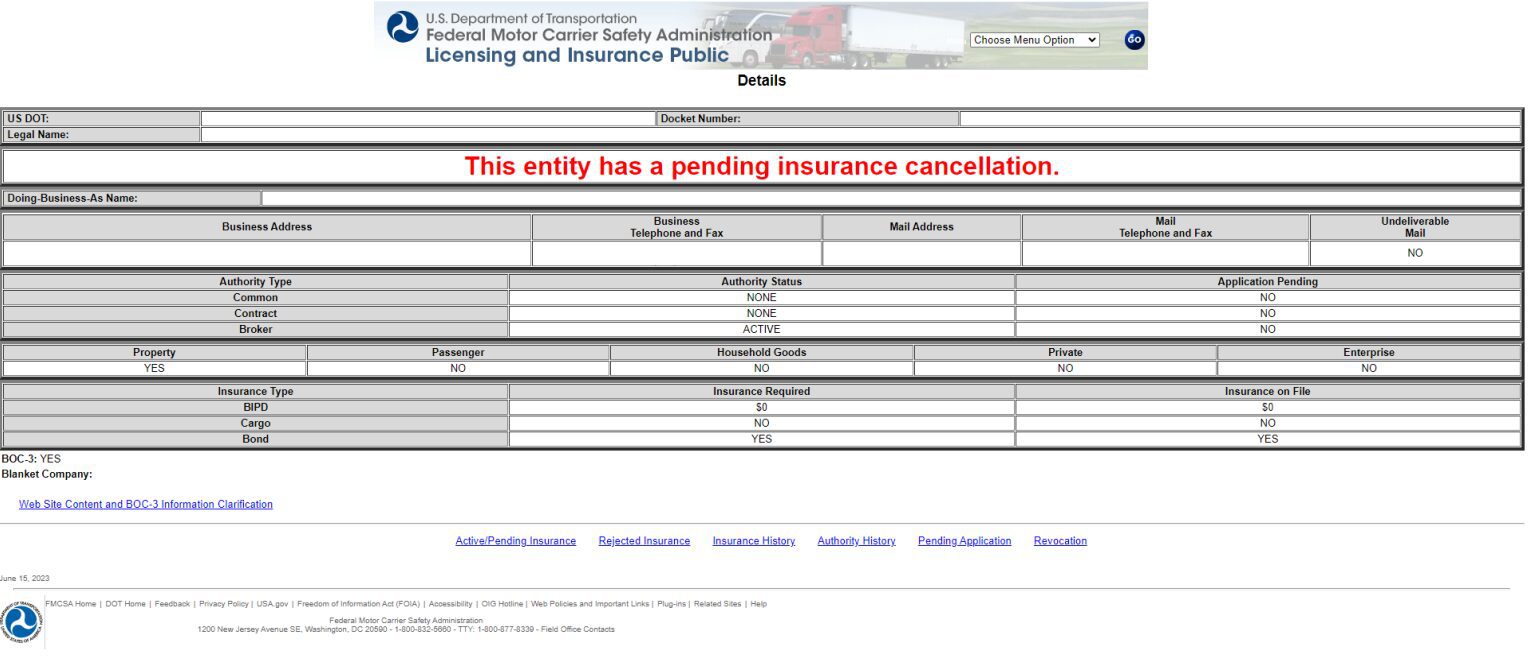

Another blaring red flag might be if you pull up their listing and see this:

Pending insurance is not an immediate no-go. This warning will always appear when insurance is within 30 days of expiring. So, if you click into the Active/Pending insurance highlighted on the first screenshot and see that their insurance is just coming up on the year that it naturally expires, there is a good chance they are in the process of re-upping.

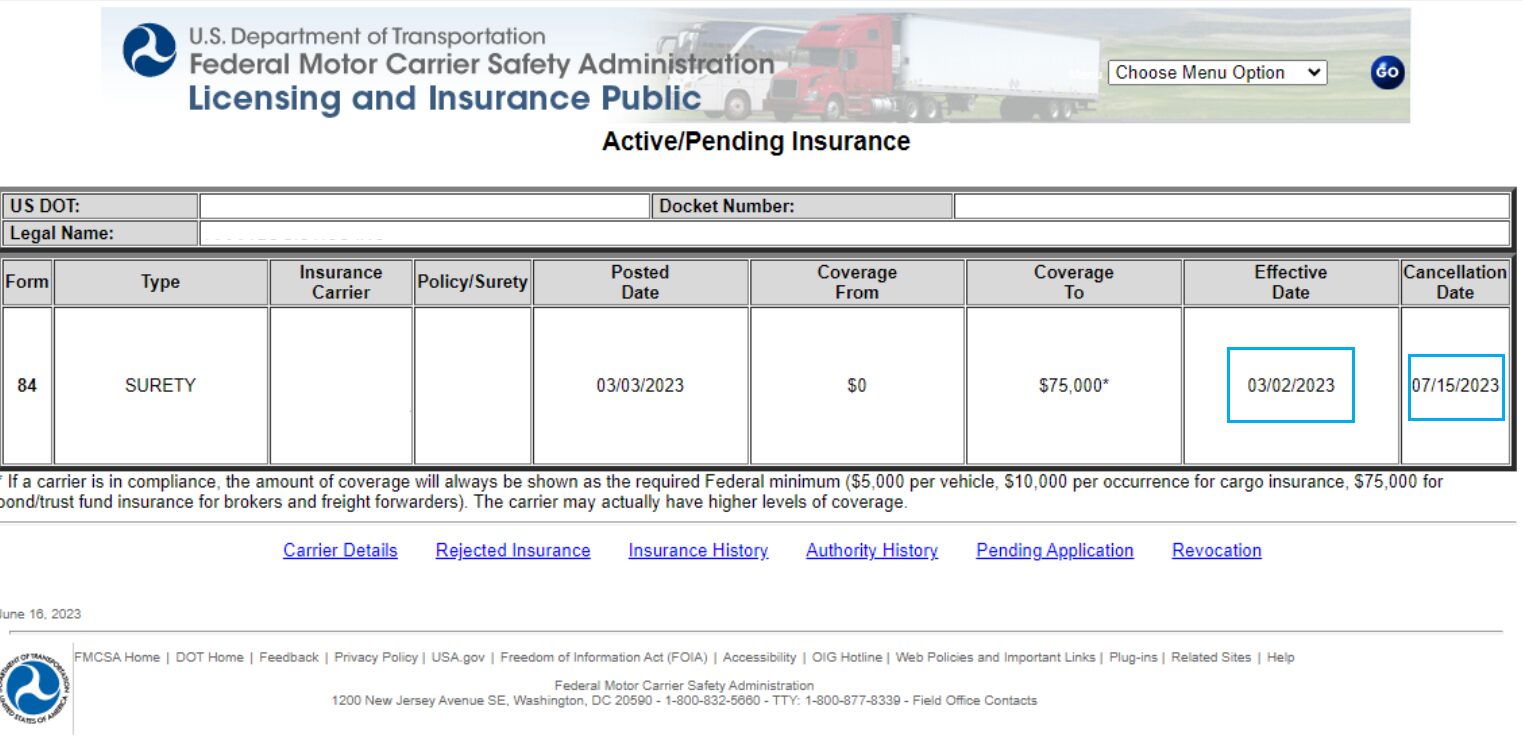

However, something we have been seeing a lot more of recently is something akin to this:

Where insurance is set to cancel only a few months after the effective date. It helps to confirm by viewing their Authority History (also highlighted on the first screenshot), but 11 times out of 10, you will find that the company has only been in business for about this long. A common trend with these is that they will post their loads 25%-50% higher than the common rates and then fall off the face of the planet once their insurance is up, leaving a graveyard of unpaid bills in their wake.

Should you find you have hauled a load for such a company, you can get information on their bond by clicking on the Insurance Carrier field (removed from this screenshot for privacy’s sake) to file on. We always recommend checking in with your RM & A/R Manager before taking this step, as A/R might have additional info on the company from other clients, or they may start ramping up collection efforts on your behalf.

RESOURCE CENTER

Learn More About Invoice Factoring

9 Signs It’s Time to Switch Factoring Companies

Most businesses don’t switch invoice factoring companies because they’re unhappy. They switch because they eventually discover what their agreement actually…

10 Questions to Ask Before Choosing an Invoice Factoring Company

Waiting 30, 60, or even 90 days for customers to pay can make it hard to cover payroll. It can…

Invoice Factoring Without Long-Term Contracts: Why Flexibility Matters

Many business owners turn to invoice factoring because they need working capital now, not because they want to commit to…